|

|

|

||||

Reviving Private Investment in India: Determinants and Policy Levers

AKSHATA KALLOOR, Project Associate, NIPFP. email:akshata.kalloor@nipfp.org.in

|

Private investment has played a central role in accelerating growth in India since the mid-1980s when India began liberalizing its economy. But private investment has slumped in the last three years leading to a slowdown in economic growth and its revival is vital for accelerating India’s growth rate on a sustained basis. India also has a huge public infrastructure deficit and declining public investment. Public investment typically crowds in private investment. The banking sector faces a huge problem of non-performing loans (NPLs), some of which emanate from stalled infrastructure projects. As a result, credit to the private sector has slowed down hurting private investment.

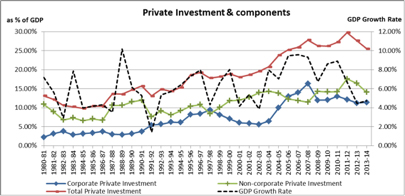

Corporate investment peaked in 2007-08 at around 16% of GDP, but has since fallen to under 10% of GDP, as credit to the private sector slowed down and banks started facing NPL problems. Non-corporate investment which includes housing, real estate and small and medium enterprises as well as agriculture continued to rise to around 18% of GDP in 2011-12 due to high growth and continued government spending which was financed by high fiscal deficits. But as growth slowed and fiscal spending was tightened it too has dropped sharply.

This paper analyzes the determinants of aggregate private investment and its components – corporate and non-corporate private investment for the period 1980-81 to 2013-14 using the old GDP series as the new series is not available and is under review. The paper finds that the key determinants of private investment are the size of the public sector capital stock, the real effective exchange rate, output gap and the availability of credit to the private sector. When we break it down further, private corporate investment is significantly explained by the real exchange rate and the availability of credit to the private sector whereas for non-corporate investment, public investment is the most significant variable - as it crowds in private investment. Real interest rate has no significant effects on investment.

The estimated model is used to explore different policy options for reviving private investment. Simulations show that if India increases public investment by 5% of GDP, depreciates the real exchange rate by 10-15% and fixes the bad loan problems in the banking sector so that credit growth to the private sector is restored India can increase its GDP growth rate by at least 2% points on a long run sustained basis and achieve 8% plus GDP growth.

The five simulation exercises conducted were:

Simulation 1: Public Investment increased by 5% of GDP.

Simulation 2: Public Investment increased by 5% of GDP but paid for by borrowing from the banking system, thereby, reducing credit to the private sector by the same amount.

|

Simulation 3: Public Investment increased by 5% of GDP and the real exchange rate is depreciated by 10%.

Simulation 4: Public investment increased by 5% of GDP, real exchange rate depreciated by 10% and credit to private sector grows by at least 10% of GDP.

Simulation 5: Public investment increased by 5% of GDP, real exchange rate depreciated by 20% and credit to private sector grows by at least 15% of GDP The estimated GDP growth rate under various simulations are shown below:

Table: GDP growth rate under different policies

If India has to achieve 8% plus GDP growth on a sustained basis, it must revive private investment well over 25% of GDP – closer to 30% of GDP. Together with public investment of around 14-15% of GDP India needs an investment rate of over 40-45 % of GDP for the next twenty years.

The role of public investment is critical as it helps build public capital needed for the provision of basic services but it also helps draw-in more private investment. Public investment must be increased by around 5% of GDP from its current level of under 10% of GDP and much of the increase must come from investment by the state and central government – not just by the public sector undertakings.

Another key variable is the real exchange rate which was kept artificially appreciated for much of the 1980s, through import controls. With liberalization after the 1991 foreign exchange crisis, the real exchange rate found its competitive level. But after the global economic crisis it was again allowed to appreciate as capital flooded into India as the developed world resorted to unprecedented QE programs. Our results show that a 10% real depreciation would add almost 0.3% points to GDP growth and a 20% depreciation would add almost 0.5 % point to GDP growth, ceteris paribus.

The growth of credit to the private sector is another critical variable and its growth must rise above 10% of GDP to generate more investment. Large fiscal deficits crowd out credit to the private sector. But lately what has constrained credit growth are the NPL problems in the banking system used to finance uncompleted PPP infrastructure projects which must be addressed. If credit to private sector growth is at least 10% of GDP, India’s growth rate increases by around 1.7% of GDP and to almost 2.2% points if it rises to 15% of GDP.

Our analysis shows that to achieve 8% plus growth, India must increase public investment to around 14-15% of GDP, depreciate the real exchange rate by at least 10% and increase the growth of credit to over 10% of GDP. This is the policy package that many fast growing countries – such as China followed over a 20-30 year period to sustain double digit growth.

References

Chhibber, Ajay and Akshata Kalloor. (2016). Reviving Private Investment in India: Determinants and Policy Levers. NIPFP Working paper No. 181.

1 1% was added for productivity improvements.

|

|

National Institute of Public Finance and Policy • New Delhi, India • URL: www.nipfp.org.in • Tel: +91 11 26569286, 26852398 |

|